Using Internet Banking (Electronic Financial) Services

① Signing up for Internet Banking

Internet banking services are also known as electronic financial services, as it allows you to use banking transaction services using a PC or laptop connected to the internet. You may conduct other personal banking such as account-checking or money transfer during banking or non-banking hours without visiting the bank. Lower fees are charged than that when using a bank teller, and you can enjoy lower interest rates when you sign up for savings products such as savings deposits and installment savings.

To sign up for internet banking, you need to go to your bank where you already have an account with some forms of personal identification (such as your alien registration card, passport or resident registration card) and apply for internet banking service. It is recommended to sign up for internet banking service when first opening your bank account. It is more convenient to set the ID required for internet banking access before visiting the bank.

After you sign up for internet banking, you will need to download a computer program called Personal Digital Certificate, which functions as your digital ID, from your bank’s internet website at home. Some banks provide internet banking services in multiple languages such as English, Chinese, Vietnamese, and Russian to enhance user convenience.

인터넷뱅킹(전자금융 서비스) 이용하기

① 인터넷뱅킹 가입

인터넷뱅킹은 인터넷이 연결된 컴퓨터나 노트북을 이용해 은행거래를 하는 것으로 전자금융 서비스라고도 합니다. 은행에 갈 필요 없이 은행 영업시간과 상관없이 계좌 조회나 이체 등 다양한 은행 업무를 편리하게 볼 수 있습니다. 은행 창구를 이용할 때보다 수수료가 저렴하며, 예금, 적금 등 저축상품을 가입할 때 금리 혜택도 받을 수 있습니다.

인터넷뱅킹을 하려면 먼저 신분증(외국인등록 증, 여권, 주민등록증 중 하나)을 가지고 은행에 가서 인터넷뱅킹 이용 신청을 해야 합니다. 처음 통장을 만들 때 한꺼번에 인터넷뱅킹 거래를 신청하는 것이 좋습니다. 은행 방문 전 인터넷뱅킹 접속에 필요한 아이디(ID)를 미리 정해 놓으면 편리합니다.

은행에서 인터넷뱅킹 신청이 끝나면, 집에서 은행 홈페이지에 접속해 공동인증서나 금융인증서 가운데 하나를 선택해 발급받아야 합니다. 일부 은행은 외국인이 영어, 중국어, 베트남어, 러시아어 등 모국어로 편리하게 인터넷뱅킹을 이용하도록 외국어 지원 서비스를 제공하고 있습니다.

How to Sign Up for Internet Banking 인터넷뱅킹 가입 방법

1. Visit a bank branch where you have an account - Take a ticket and wait for your turn.

1. 은행 방문 - 번호표를 뽑아 자기 순서를 기다립니다.

2. Fill out an application form and create your user ID - Fill out an internet banking application form as instructed and create your user ID.

2. 신청서 작성 및 이용자 ID 정하기 - 은행원의 안내에 따라 신청서를 작성하고 인터넷뱅킹 접속에 필요한 아이디(ID)를 정합니다.

3. Set maximum transfer amount and create your PIN for money transfer - Create your PIN for money transfer authorization and set the oneday/one-time maximum transfer amount that can be sent to another account. The PIN for money transfer is used when sending money to another account using internet banking. The one-day maximum amount limits how much money you can send from your account in a single day.

Similarly, the onetime maximum amount limits how much money you can send from your account at one time.

3. 이체한도와 비밀번호 등록 - 1일/1회 이체한도 및 자금이체 비밀번호를 설정합 니다. 이체한도는 하루 또는 1회에 다른 계좌로 보낼 수 있는 금액의 한도이고, 자금이체 비밀번호는 인터넷뱅킹을 이용해 돈을 보낼 때 사용합니다..

4. Choose either Security Code Card or OTP - Your password for internet banking is used to prevent fraud and other criminal activities involving your bank account. You can use either a number on your security code card or a code (number) generated by OTP (One-Time Password) as your password.

4. 보안카드나 OTP 중 선택 - 인터넷뱅킹을 이용할 때마다 다른 사람이 본인의 계좌에 접근하지 못하도록 비밀번호를 입력해야 합니다. 이때 필요한 것이 보안카 드나 OTP입니다. 둘 중 하나를 선택해서 사용하면 됩니다.

Handy Tips for Using Financial Services 금융생활 꿀팁

If you use an electronic bankbook, you can enjoy preferential incentives!

The bank offers preferential incentives such as reduced fees and favorable interest rates to customers who sign up for an electronic passbook without being issued a paper-printed passbook. If you are going to conduct financial transactions mainly through internet banking or mobile banking, you can use an electronic bankbook and enjoy such incentives.

전자 통장을 이용하면 우대 혜택을 받을 수 있어요!

은행은 종이 통장을 발급받지 않고 전자 통장에 가입하는 고객에게 수수료 감면, 금리 우대 등 우대 혜택을 제공합니다. 자신이 주로 인터넷뱅킹이나 모바일뱅킹을 이용해 금융거래를 할 계획이라면 전자 통장을 이용하는 것도 좋은 방법입니다.

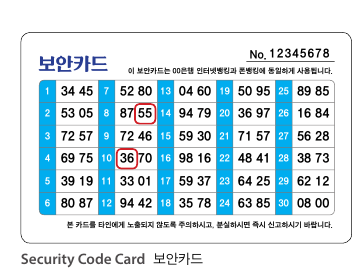

② Security Code Card and OTP

A Security Code Card is a card the size of a business card with security codes printed on it. A typical security code card has 30 to 35 security codes, each consisting of a four-digit number.

When using internet banking services, you need to enter two separate numbers on the security code card.

(For example) You may be asked to enter the first and the second digits of the tenth (10th) security code and the third and the fourth digits of the eighth (8th) security code.

OTP is a small electronic device that generates a security code whenever using internet banking.

An OTP-generated security code works only for one single transaction. Because it generates a single six-digit number for you each time you press the OTP button, it prevents others from using it. You must enter the six-digit number on the screen when you are asked for it. OTP issued by one bank can be registered for transactions at multiple banks.

A security code card is usually given to you free of charge when you sign up for internet banking.

However, numbers on the security code card are given in advance, while an OTP device generates unlimited new security numbers each time you switch it on. Never lend or show your security card or OTP to anyone. If you lose it, you should report it to the bank immediately, cancel the ex-

isting one, and then be reissued with a new one.

② 보안카드와 OTP

보안카드(Security Code Card)는 비밀번호가 인쇄된 명함 크기의 카드입니다. 보통 4자리 숫자 30~35개가 인쇄되어 있습니다. 인터넷뱅킹을 이용할 때 컴퓨터 화면에서 요구하는 비밀번호 2개 번호의 앞 2자리와 뒤 2자리 숫자를 입력하면 됩니다.

예) 보안카드 10번(앞 2자리), 보안카드 08번(뒤 2자리)

OTP(One Time Password)는 일회용 비밀번호가 그때그때 자동으로 만들어지는 기계입니다.

버튼을 누를 때마다 새 번호가 만들어지므로 비밀번호 유출로 인한 피해를 예방하는 데 효과적 입니다. OTP 화면에는 6자리 숫자로 된 비밀번 호가 나타나며, 컴퓨터 화면에 이 숫자를 입력하면 됩니다. 하나의 은행에서 발급받은 OTP를 여러 은행에서 등록하여 같이 사용할 수 있습니다.

보안카드는 보통 무료로 발급해 주지만, 보안번 호가 미리 인쇄되어 있어 매번 비밀번호가 새로 생기는 OTP보다 보안에 취약합니다. 보안카드나 OTP는 절대로 다른 사람에게 빌려주거나 보여주면 안 됩니다. 만약 분실했을 경우에는 바로 은행에 신고해 폐기처리한 후 재발급받아야 합니다.

댓글